Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Bonds

The Swiss National Bank has once again lowered its key interest rates to 0%, and annual yields on 10-year Swiss government bonds are also below 0.5%. After deducting costs, it is no longer possible to generate returns with AAA-rated fixed-income investments. On the contrary, if inflation picks up again, as it did in 2022, and yields rise, losses are inevitable. We have therefore made a strategic adjustment in our actively managed mandates (PRIMUS-ACTIVE and PRIMUS-ETHICS) with a high bond allocation (income). In the bond segment, we have reduced the strategic exposure. At the same time, we have tactically increased credit risks somewhat. Although we do not currently anticipate any acute inflationary pressure or rising yields in Switzerland (see following section), we are implementing this adjustment now with the aim of achieving higher returns and continuing to generate income in the fixed-income segment. As 2022 also demonstrated, higher inflation is difficult to forecast, given that it is typically driven by extraordinary events.

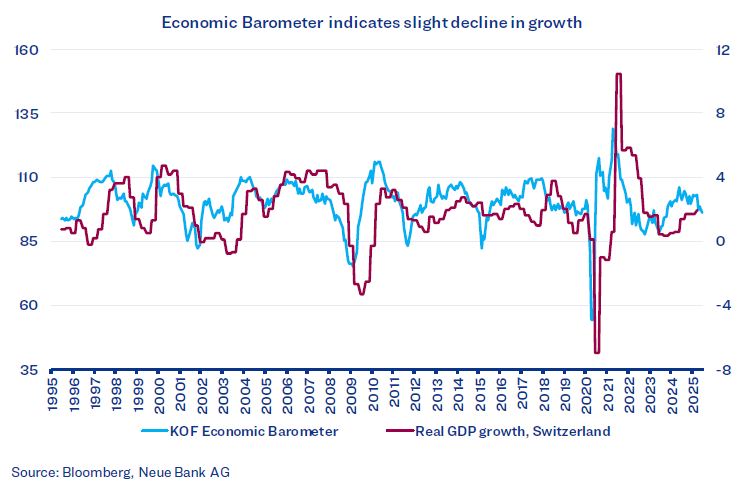

Economy

The economic outlook in Switzerland has deteriorated slightly, but positive growth rates can still be expected.

At present, there is certainly no sign of runaway inflation. The recent decline in the KOF Economic Barometer is partly due to the fact that growth in the first quarter was driven by orders and deliveries to the United States being brought forward in anticipation of the announced tariffs. This growth subsided in the second quarter. Trade policy and potential tariff increases will shape the economic outlook in the near future.

Equities

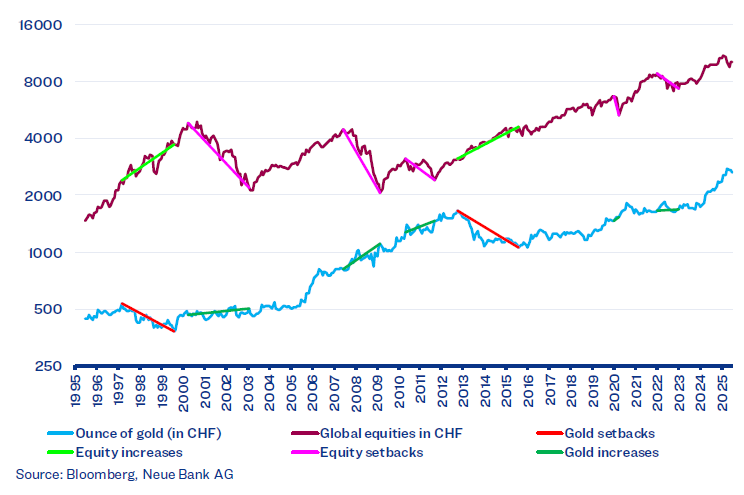

We are investing part of the funds freed up by the reduction of our strategic bond allocation in equities. While the risk of somewhat higher short-term fluctuations cannot be dismissed, this risk is lower over a long-term horizon.

Taking inflation into account, bond investors have also needed considerable patience before being able to recoup their losses. Anyone who invested in the bond index at the end of 1936 and liquidated their positions in 1974 earned nothing in real terms (after inflation), despite a holding period of 38 years. However, thanks to generally much lower inflation rates, CHF investors were still more successful than their USD or European counterparts, as the respective countries often attempted to “inflate away” their debt and therefore tolerated relatively high inflation rates. Swiss equity investors, by contrast, had to endure a real loss for a maximum of 23 years and achieved an average annual real return of 5.6% over 100 years, compared with 2.1% for bond investors. Given that not all investors have a long investment horizon or the same capacity to cope with asset fluctuations, we have taken these factors into account in our adjustments.

Alternative investments

We have reallocated another portion of the freed-up funds into gold and introduced a new strategic allocation for income mandates. Many BRICS countries are seeking to reduce their dependence on the USD and are therefore increasing their gold holdings, which lends support to gold investments.

During equity market crises, gold often serves as a safe haven. In phases when gold consolidates, equities have regularly shown a positive trend over the past 30 years. This negative correlation has a favourable impact on portfolio risk, as it helps to reduce volatility. This has led us to include this asset class – even though it is more volatile when viewed in isolation – instead of less volatile bonds. Overall portfolio fluctuations should not increase significantly as a result.

Currencies

Investors who think in Swiss francs (CHF) and invest abroad often face the challenge that the appreciation of domestic currencies can negatively impact foreign investments. It is therefore highly advisable to manage foreign currency exposure. For fixed-income investments, we generally avoid taking on foreign currency risks. For equity investments, we implement hedging of up to 5% of the portfolio value per foreign currency. Given that global equity indices comprise up to 70% USD-denominated stocks, and a misjudgement at such a weighting could negate the benefits of good stock selection, we have opted for this restriction. At present, we have fully or partially hedged all major currencies (USD, EUR, JPY, and GBP) in CHF portfolios.