Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

“Arbitrariness damages trust”

Economy

The surprisingly weak number of new jobs created (non-farm payrolls) shows that the US economy is more vulnerable to the trade war than the White House would like. The real negative surprise was not so much the announcement of the July figures, but rather the significant downward revisions for the two previous months. The publication of the disappointing labour market report had immediate consequences for the employment of Erika McEntarfer, head of the US Statistics Bureau, who was fired by Donald Trump on the same day. His reasoning was that the data had been ‘manipulated’ to make him look bad. He also claimed that the agency had falsified figures in favour of the Democrats in the past – an unfounded allegation for which there is no evidence whatsoever. The same fate befell Fed Governor Lisa Cook, who was also to be dismissed on the basis of unsubstantiated allegations by Trump. However, Cook refused to resign, stating that there was no legal basis for doing so. The case is therefore likely to end up before the Supreme Court. This has raised new concerns about the independence of the central bank, as no president in US history has ever attempted to dismiss a member of the Fed’s board of directors. Trump has long been pressuring the Fed to lower interest rates and has repeatedly criticised Fed Chairman Jerome Powell in derogatory terms. Cook’s departure would enable Trump to fill a fourth position on the Fed’s seven-member board of directors, resulting in a majority in favour of interest rate cuts. Further evidence of Trump’s arbitrary actions can be found in his tariff policy. A US federal court recently ruled that large parts of Donald Trump’s tariffs were unlawful. By a vote of seven to four, the judges ruled that only Congress can decide on these reciprocal tariffs. Whether Trump’s arbitrary actions are part of a strategy (madman theory) or simply impulsive decisions without a clear line, characterised by personal whims and short-term advantages, remains to be seen.There is no question that these erratic decisions undermine confidence in the state and its institutions in the long term. A loss of confidence in the US would significantly destabilise the financial system, as confidence is the foundation of any financial system.

Bonds

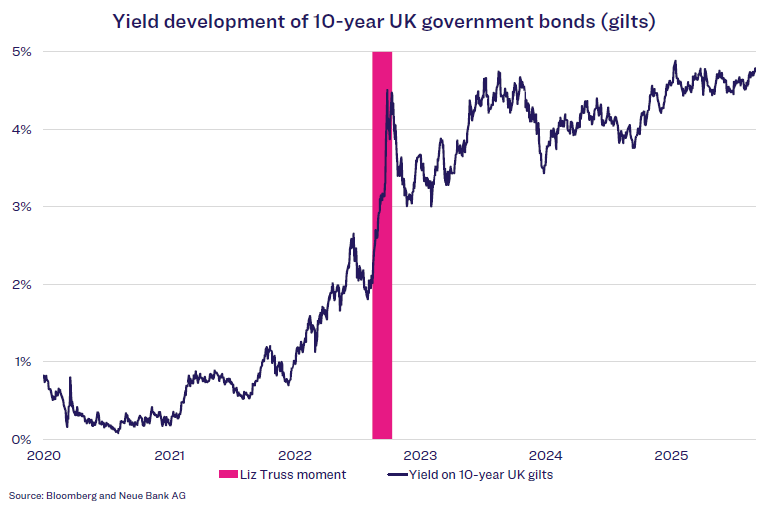

Investor confidence in a country can be gauged by the performance of its government bonds. If confidence in the likelihood of repayment declines, government bond prices fall and yields rise because buyers want higher risk premiums. The Liz Truss moment shows how quickly this can happen. In September 2022, then British Prime Minister Liz Truss and her Chancellor of the Exchequer Kwasi Kwarteng presented a debt-based tax cut programme to stimulate economic growth. Bond investors now expected a significantly lower probability of repayment, despite the UK’s good credit rating. As a result, UK government bond prices tumbled and yields skyrocketed. Both politicians subsequently had to resign.

The market for US Treasury debt securities is the largest in the world and also the Achilles heel of the United States, as Trump has discovered. After he announced the new tariff regime on Liberation Day, there was a sudden rise in yields on the US Treasury market. He quickly backtracked on the tariffs, and the situation calmed down again. This was a first warning sign of what can happen when investors lose confidence. It was not enough for a Liz Truss moment, but the bond markets remain vigilant. If Trump continues to strain confidence with his actions, the tipping point could be reached at some point, with unforeseeable consequences for the financial system. The US Treasury market remains the yardstick for the success or failure of the Trump administration.

Shares

And what about the stock markets? Why have they been so buoyant so far? Nobody wants to lose out due to misjudgement there either, but they are different in nature from the bond markets. The informational value of share prices lies in the assessment of a company’s future cash flows, which is based on a multitude of facts, trends and probabilities of their future occurrence. Trump’s actions have a certain influence, but only one among many. Currently, the probability of immense productivity gains through artificial intelligence is being played out, which is why the stock markets are trending positively despite the politically hostile environment. It is impossible to say definitively how long this trend will continue and whether this development is sustainable. However, a great deal of optimism is being priced into AI development, which could lead to sharp corrections if these expectations are not met.

Currencies

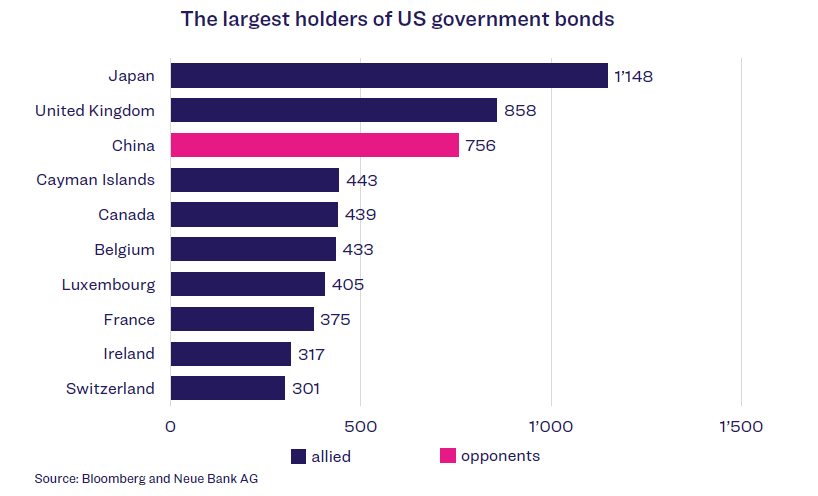

The US dollar is the world’s most important currency and thus another seismograph for confidence in the American economy. Currently, both the USD index and confidence in the United States as a reliable partner are in decline. Since taking office, Donald Trump has continuously weakened the US dollar with his erratic policies. The US dollar index, which compares the US currency with an international basket of currencies, has lost around ten per cent of its value since the beginning of the year. The balance sheet has never been worse since the turn of the millennium. Another risk for the USD comes from the holders of US government bonds. The United States’ allies hold the largest share of US Treasuries.

Friendly countries tend to hold more bonds among themselves because close political and military ties reduce the likelihood of conflict and expropriation. However, Donald Trump’s confrontational approach is damaging trust and, consequently, relations. If allies were to significantly

reduce their holdings, this would likely result in further losses for the greenback.

Alternative investments

With a 40 per cent increase since the beginning of the year, the precious

metal silver has exceeded the USD 40 per troy ounce mark and reached its highest level since 2011. Strong industrial demand in particular has driven up the price. Photovoltaic production accounts for more than 30 per cent of annual production. However, the weak US dollar and political uncertainties are also boosting global demand. In China alone, the import volume of silver bars rose by around 25 per cent in the first half of the year. Silver has stepped out of gold’s shadow, supported by strong industrial demand, scarcity and political unrest.