Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

The economy

The Trump administration has no less in mind. Trump is determined to make America great again. To achieve this, the plan is to reduce trade deficits or – even better – turn them into surpluses. The plan is therefore to reduce imports of foreign goods by introducing tariffs. At the same time, the intention is to increase the attractiveness of the location through tax cuts and to initiate re-industrialisation. This serves the intention of making the US economy more independent and resilient, which are certainly noble goals. However, aside from the lack of diplomatic communication style of the US government, there are conflicting goals that make implementation difficult. The tariffs, which are intended to strengthen domestic industry, increase costs and place a burden on the consumer, who accounts for around 70% of gross domestic product (GDP) in the USA (in the eurozone, for example, this figure is only around 55%). Reconstruction focusing on traditional industries and pressuring companies to relocate their production to the United States will lead to inefficiencies. Tax cuts are intended to stimulate consumption and investment, but at the same time are a burden on the budget. With debt at 120% of GDP, the USA already has a level of debt never reached in peacetime. This list does not claim to be exhaustive, but it does show that the challenges to success are – to put it mildly – not few.

Bonds

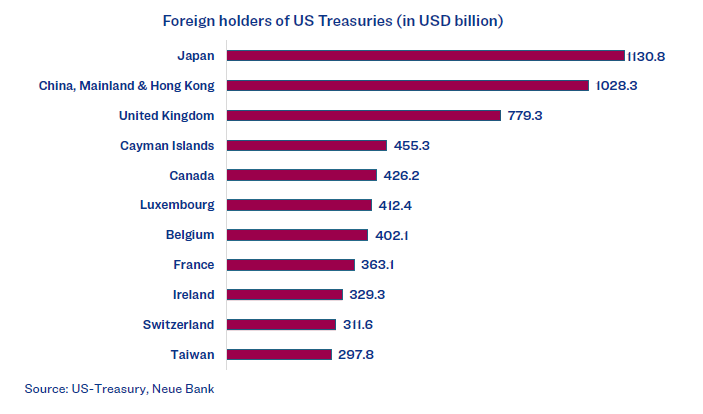

It is precisely the high level of debt that gives creditors a certain degree

of bargaining power. We therefore take a look at the largest investors:

China and Japan are among the top holders of US government bonds. As a result, they could exert pressure on the USA in the context of the current tariff disputes. Some market commentators believe they have identified the Achilles’ heel of the USA here. A massive sale of these bonds could cause interest rates in the USA to rise and make the already high US debt servicing even more expensive, which would put the USA under pressure. Nevertheless, there are good reasons why these countries would not simply sell off their holdings. Such a move could not only destabilise the financial market but also damage their own economies. The pressure to sell would cause their currencies (JPY and CNY) to appreciate, which would make their exports more expensive and cause economic problems. In addition, US government bonds are an important reserve for both countries, which they do not want to give up easily as they serve as safe and liquid investments. In addition, the US Federal Reserve could intervene (it has reduced its Treasury holdings by over USD 1’500 billion since 2022) to stabilise the markets, which would mitigate the impact of a sale. And last but not least, such a move could significantly exacerbate geopolitical relations between the US, China and Japan – a risk that these countries also want to avoid. In short, while China and Japan have some negotiating power, the risks of a massive sale of US Treasuries are so high that escalation seems unlikely.

Equities

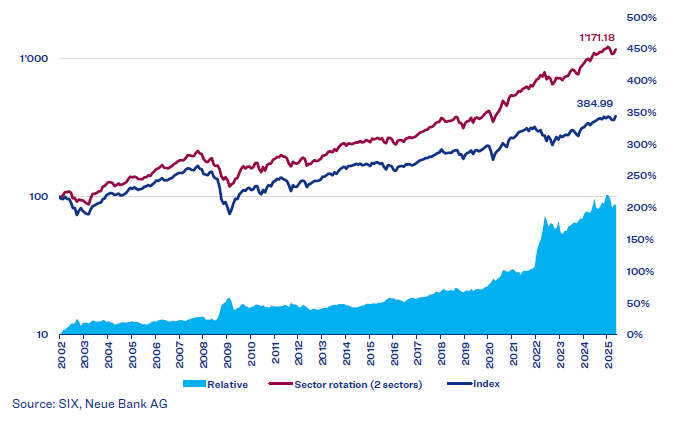

In addition to a positive return, the aim of an equity strategy is also to outperform the benchmark index. In order to ultimately achieve a positive performance, the longest possible time horizon is required. Over any 15-year period since 1975, the global equity market – even measured in CHF (the strongest of all currencies) – has never posted a negative performance. There are various methods for outperforming the market. One of these is to overweight equities compared to the benchmark. We manage this on the basis of our Neue Bank Ampel risk management system, which we also publish monthly in ‘Our Opinion’. In the past month, the assessment has improved and is currently light green (slightly bullish), which results in a slightly increased equity exposure. In addition to the different weightings of asset classes, we also utilise other strategies. For example, we are positioning ourselves in our favoured sectors:

We take various measurements to select the sector indices. The aim is to be invested in cyclical stocks as much as possible during an upswing in order to benefit from above-average price gains. Conversely, we aim to switch to more defensive stocks as early as possible during prolonged corrections. We are currently invested in ETFs on communication services (e.g. Meta, Alphabet, Walt Disney or Deutsche Telekom) and financial investments (banks, insurance companies and financial service providers). We implemented this strategy towards the end of last year. The chart above shows how a corresponding ‘rotation portfolio’ would have behaved with the rules we defined.

Alternative investments

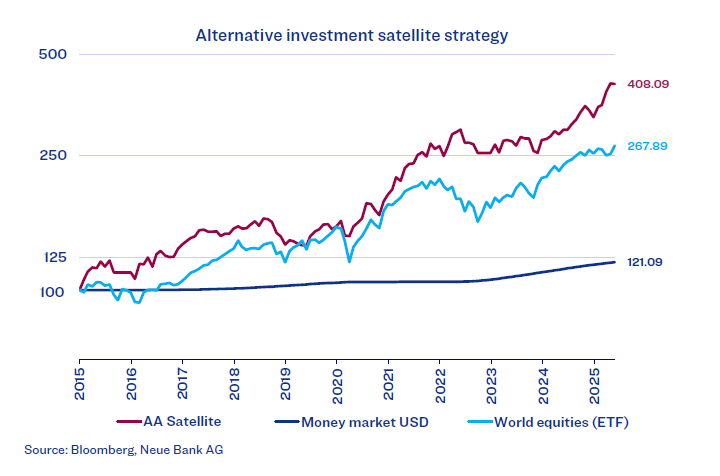

In addition to defensive core investments, which should generate the most stable returns possible regardless of the performance of bond and equity markets, we also pursue an active trading strategy with the satellite investments. In addition to the current investment in gold, ETFs on commodities, real estate, listed private equity and cash are also available as alternatives.

We have been invested in gold again since the beginning of February, and it has gained around 18% since then. As the above comparison shows, this strategy has even outperformed equities over the last 10 years.

Currencies

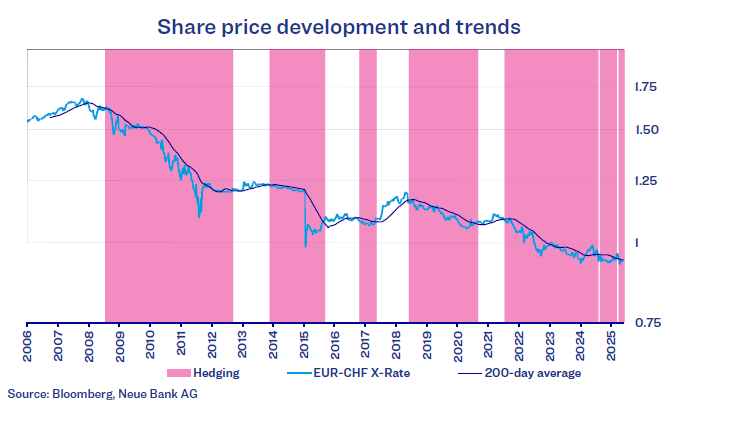

In Germany, the debt brake has recently been relaxed, while in Switzerland it is being stubbornly adhered to. This is one of the reasons why the Swiss franc (CHF) is extremely strong, especially against the euro (EUR). In order to limit currency losses, we have also developed a trading system that shows us when currency hedging should be undertaken:

A look at the EUR/CHF exchange rate over the last almost 20 years shows how much the EUR has weakened. At its peak in 2007, EUR 1.00 still fetched over CHF 1.68, but now it is not even CHF 0.95, i.e. well over 40% less. It can therefore be worthwhile to hedge the EUR exposure temporarily. Depending on the signal, we hedge in all major currencies (USD, EUR, JPY and GBP).