Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Equities

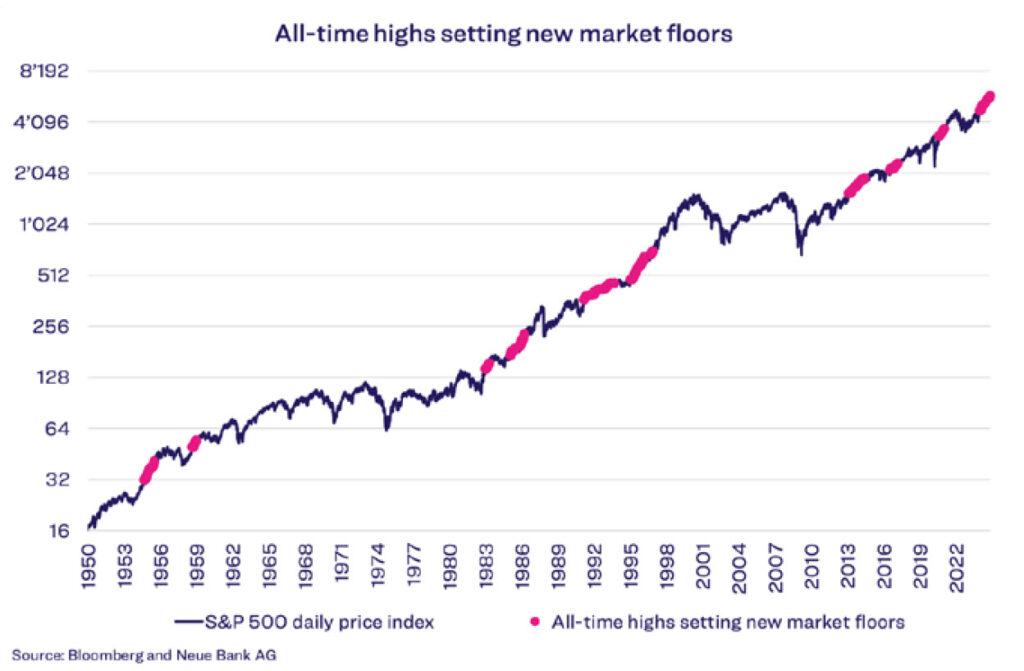

In light of the current highs on the equity markets, does it still make sense to invest, or is it better to wait for a possible major correction? Clients ask this question very often. No one can give an answer as to the best time to enter the market, since no one knows where prices will be in the future. Investors who set price targets for corrections may run the risk of missing the entry point completely if the price target is not reached. On the other hand, investors should not be scared away by equity markets that continue to rise. Historically, equity markets have risen over the long term, reaching new highs time and again. The following chart shows the long-term performance of the US equity market S&P 500 with market floors, which are defined as all-time highs from which the market never fell more than 5%.

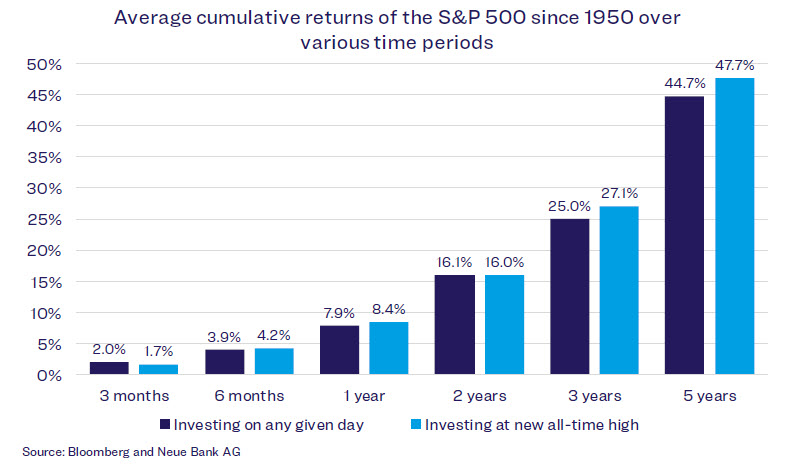

The next chart likewise illustrates that, historically speaking, investing at an all-time high has not led to worse performance in the long term than investing on any other random day. On the contrary, in four out of six time periods considered, a slightly better return was actually achieved. Here, “investing on any given day” represents the average of all future returns for the time intervals over 3 months, 6 months, 1 year, 2 years, 3 years, and 5 years between 1950 and 2024, while “investing at new all-time high” represents the average of the ongoing returns generated from each new high of the S&P 500 over the same time intervals.

PRIMUS investment plan

Of course, there have also been negative market phases in the past that lasted several years. Investors who invested before the financial crisis in 2007, for example, had to wait several years until the initial level was reached again. To mitigate such situations, it is possible to invest the investment amount in several tranches over a given period of time. This reduces the risk of investing the entire investment amount at an unfavourable time. With the PRIMUS investment plan, we offer such a plan at preferential conditions. If you are interested, our client advisers will

be happy to assist you.

Economy

The preliminary Purchasing Managers’ Indices (PMI) for the US have exceeded expectations. The Composite PMI, which includes both services and manufacturing, remains comfortably in the growth zone. According to current GDP estimates, the US economy is likely to have grown by 2.8% in the third quarter. However, the US figures are annualised, which makes the figure look more impressive. If GDP were broken down into non-annualised quarterly growth, the figure would be 0.7% – which is still impressive by international standards. The US economy is therefore still proving to be more robust than many expected. The picture is very different in the Eurozone, where the economic recovery is still making only sluggish progress. The GDP estimate for the third quarter is 0.4%, continuing to lag significantly behind US growth.

Bonds

The US yield curve has become significantly steeper recently, as longerterm interest rates have risen faster than short-term rates. The International Monetary Fund (IMF) has taken a closer look at this movement and identified a unique feature in the drivers of this interest rate movement. Steepening can be driven by an assessment of higher inflation (bear steepening) but also the opposite, falling inflation (bull steepening). In bear steepening, long-term yields rise faster than short-term yields. The markets then price in higher risk premiums for long-term interest rates, given the increasing uncertainty about the development of inflation and monetary policy. Bull steepening, on the other hand, expects an easing of monetary policy. Steepening of the yield curve is caused by a

faster fall in short-term interest rates. But in that scenario, long-term interest rates also fall and expected inflation declines, which favours a lower risk premium for long-term yields. A new pattern has recently emerged in the distribution. Short-term yields have fallen, while longterm

yields have risen. This results in a mix of bull and bear steepening. As with bull steepening, expected inflation has fallen, but at the same time risk premiums have risen in the longer term (bear steepening). The problem here is that in the bear case, long-term bonds lose significant value. In the bull case, on the other hand, gains are generated thanks to falling yields. If this trend of falling short-term interest rates and rising long-term interest rates were to continue, this could unsettle investors and lead to more volatile markets.

Currencies

“The reports of my death are greatly exaggerated,” the writer Mark Twain is said to have said when a newspaper mistakenly published an obituary of him while he was still alive. If the US dollar could speak, it would probably say the same. Time and again, the US dollar has been predicted to soon lose its role as the world’s reserve currency – and the prophets of doom have always been wrong. The greenback still accounts for about 59% of global currency reserves, followed by the euro at 20% and the JPY at 6%. But now a new rhetorical attack on the reserve currency has begun. At the meeting of emerging economies (BRICS summit) in Kazan, Russia, calls were made to overturn the global financial architecture. Putin and Xi in particular provided arguments for a decline of the dollar and the dominance of emerging markets. However, the reality is different, and a financial order dominated by emerging markets is not imminent. The fact remains: investors, whether private or central banks, need security, a large supply and liquidity, i.e. lively trading. Only the US dollar (and to a lesser extent the euro) currently offers this combination. The USD accordingly has a network effect. People tend to prefer a currency that is accepted by the masses.

Alternative investments

Donald Trump has discovered his love for bitcoin. While during his term as US president, he declared that bitcoin was not money and would only promote illegal markets, he has apparently done a complete U-turn. At the world’s largest bitcoin conference in the US state of Tennessee, he promised to create a national bitcoin reserve for the United States if re-elected. The crypto-friendly statements boosted bitcoin and drove the price towards all-time highs. How seriously he means what he said is questionable. In this case, his intention could be to win the votes of the

crypto community. If he is elected, this plan would not be set in stone, and Donald Trump could quickly change his mind. As a consequence, the bitcoin price could plummet again.