Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Economy

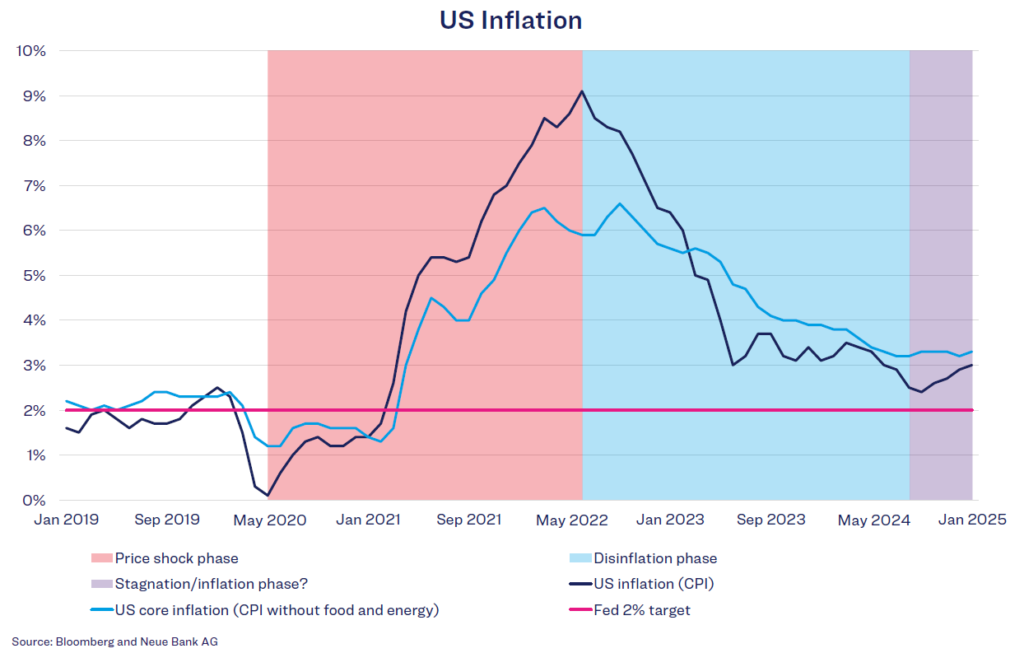

“I’ll be back” – Arnold Schwarzenegger became a legend with this quote as the Terminator. The iconic line could also apply to inflation in 2025, which has the potential to make a comeback. So far, the US Federal Reserve has failed to push inflation further towards its 2% target. In January, the core inflation rate (excluding food and energy prices) rose by 0.4% over the previous month – more than economists had expected and twice as much as in December. As a result, the annual rate climbed to 3.3% and has barely moved since mid-2024. A study by the International Monetary Fund (IMF) on historical price shocks reveals a worrying pattern: After an initial decline, inflation often tends to flare up again. The IMF economists reached the following conclusion: “Inflation fell significantly within the first three years after the initial shock but then stagnated at a high level or accelerated again.”

The US economy is currently in precisely this critical phase. The inflation trend is proving to be “sticky” – stubborn and persistent. In the second half of 2024, US economic output grew above its potential rate. Strong economic data, a robust labour market, and stable consumer spending suggest that growth of over 2% is also expected for the current quarter. This economic strength is the main reason for inflation’s continued persistence. Additional price pressure could arise from President Trump’s protectionist policies. His proposed tariffs and immigration restrictions could drive up supply-side costs, while pro-growth measures such as tax cuts and deregulation could further fuel demanddriven inflationary pressures. In an economy already operating at full capacity, such measures are likely to give inflation an additional boost. As a result, inflation remains a key factor that will continue to keep markets on edge this year.

Equities

Since the election of Donald Trump, the US equity market has struggled to gain momentum after the brief “Trump bump”. Since the start of the year, it has recorded a slight decline, with US equity markets falling well short of the optimistic forecasts made by many financial experts. At the end of 2024, analysts had expected US markets to significantly outperform global markets in 2025 – but so far, the opposite has been true. Other regions are showing much stronger growth, such as the Swiss equity market, which, with its defensive characteristics, had already gained more than 10% by the end of February, clearly outperforming the US. A key reason for the weak performance of US markets is the president’s unpredictable policies, which are causing uncertainty among investors. Rising inflation fears are also reviving memories of the sharp inflation surge in 2021–22 and its impact on equity markets. As long as these uncertainties persist, market conditions are likely to remain volatile.

Bonds

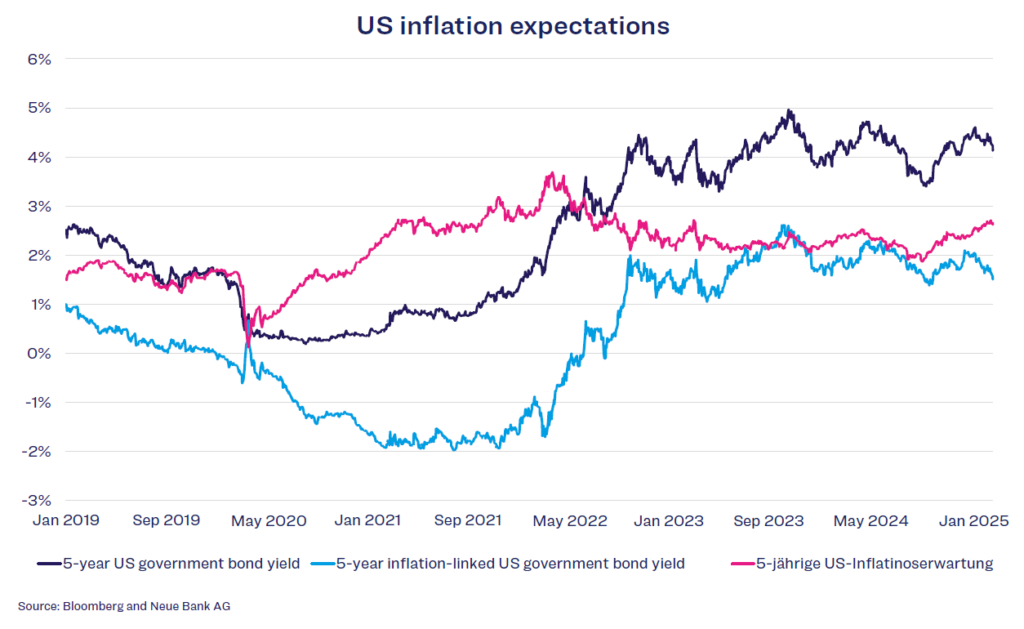

The rise in inflation risks is also reflected in 5-year US inflation expectations, which are calculated from the difference between the yield on 5-year US government bonds and the yield on 5-year inflation-linked US government bonds. Since September 2024, expectations have increased from below 2% to the current level of 2.6%.

In such an environment, inflation-linked bonds can offer a degree of protection, as their principal and coupon payments adjust in line with accumulated inflation. These securities are designed to outperform nominal government bonds when actual inflation exceeds expectations, helping to offset unexpected price pressures. At present, investors still seem to have confidence in central banks’ ability to keep inflation under control, resulting in limited demand for an additional risk premium. This creates an opportunity to build positions in inflation-linked bonds, which can add strategic value to a diversified portfolio in the current climate.

Currencies

After Canada and Mexico, the EU is now also in Donald Trump’s sights. From 1 April 2025, the US president is threatening to impose tariffs of 25% on numerous European goods. However, higher tariffs drive up the cost of imported goods and could further fuel inflation in the US. If Trump fully implements his announcements, significant price increases would be expected. In such a scenario, the US Federal Reserve would face a difficult decision: To keep inflation under control, it would need to maintain high interest rates for longer – or, in the worst case, even raise them again. The goal behind Trump’s protectionist measures is likely to be reducing US dependence on foreign goods. Fewer imports would lower demand for foreign currencies and strengthen the US dollar. At the same time, a smaller trade deficit – driven by increased exports and reduced imports – could further support the greenback. That, at least, is the president’s wishful thinking. In reality, the affected countries are unlikely to accept such measures without retaliation. Counter-tariffs could weigh on American exports while simultaneously pushing up the cost of imported goods. In the long run, an escalating trade conflict would produce no real winners. Instead, the risk of economic disruptions looms, with consequences that are difficult to predict.

Alternative investments

After a period of consolidation, gold resumed its upward trajectory, reaching a new high of USD 2,956 per ounce. This rally is particularly remarkable given that, from a historical perspective, the current market environment is not especially favourable for gold. Riskier asset classes are in high demand, while yields on US government bonds remain elevated – making gold, which generates no interest income, appear less attractive. Nevertheless, market participants who are not fully convinced by the positive outlook are turning to gold for protection. The precious metal offers a degree of security, particularly amid growing inflation fears. Analysts also recommend gold as a hedge against Trump’s unpredictable policies. Additionally, ongoing concerns about the precarious state of US government debt provide further arguments in favour of gold. Beyond this, gold has solidified its reputation in developing countries as a reliable store of value – without any real competition. Meanwhile, both the Chinese and Russian central banks are increasing their gold reserves to gradually reduce their dependence on the US dollar. Given these factors, there are currently few arguments against gold. Our momentum indicator also responded at the beginning of February, leading us to build a position in gold at the expense of listed private equity.