Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Currency

The Swiss franc was introduced as Switzerland’s national currency 175 years ago, on 7 May 1850, with the enactment of the Federal Coinage Act. However, its success in becoming the world’s most secure and strongest currency was not predetermined. During the first 50 years of its existence, it remained a weak appendage of the French Franc. It was only with the founding of the Swiss National Bank (SNB) in 1907 that it began its steady rise to become the world’s strongest currency. Switzerland remained neutral during the two world wars, which further enhanced the franc’s credibility. In the post-war period, the Swiss Confederation joined the Bretton Woods system (which linked the US dollar to the price of gold). Under this system, the Swiss franc was also pegged to the dollar within narrow bands. After the collapse of the system in 1973, the peg to the US dollar was removed, and the franc began to ‘float’ freely, i.e. traded on the market without a fixed peg. This marked the beginning of its independent monetary policy development under the control of the SNB. In the decades that followed, Switzerland developed into one of the world’s most important financial centres, and

the franc became a preferred safe haven in times of crisis. The 2008 financial crisis intensified the shift of funds to safe havens, and the franc experienced strong upward pressure. This became even more pronounced during the euro crisis from 2010, when the SNB introduced a minimum exchange rate of CHF 1.20 per euro in September 2011 to protect the export industry. A dramatic turning point came on 15

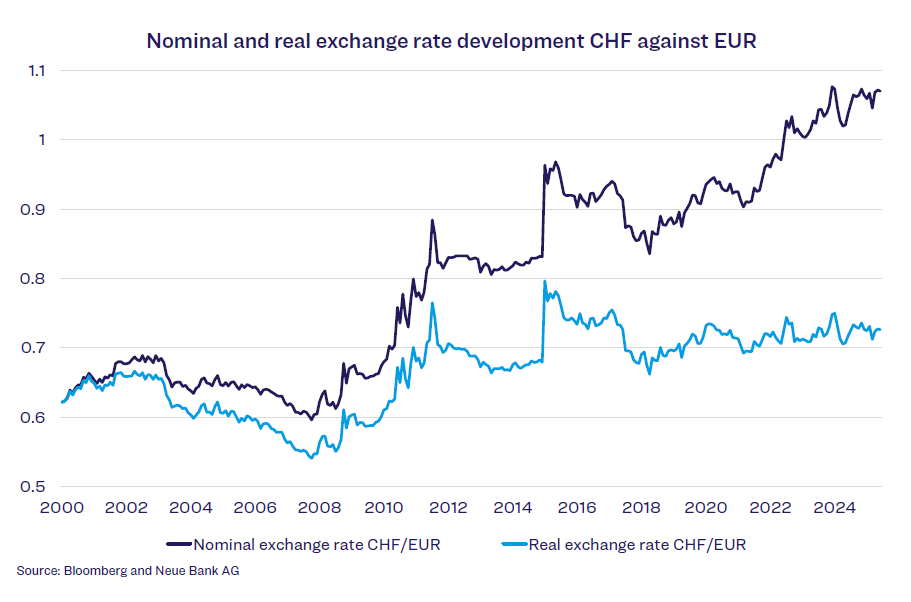

January 2015: the SNB unexpectedly removed the minimum exchange rate. The Swiss franc appreciated by up to 20 percent within a few hours. This was followed by temporary phases of weakness, but these did not last long. The upward pressure remained. The SNB even tried to tame the franc with negative interest rates – but without much success. The Swiss franc remains strong – and has once again proven to be a reliable safe haven, even in geopolitical crises (e.g. the war in Ukraine and conflicts in the Middle East). For several years now, the SNB has been more tolerant of nominal appreciation as long as inflation abroad is higher. The real exchange rate therefore takes centre stage and should remain as stable as possible. The following chart illustrates that this approach has been very successful so far:

The nominal appreciation of the CHF against the EUR since 2000 has been around 72 percent, while the real appreciation – adjusted for eurozone inflation – has only been just under 17 percent. In the past seven years, there has even been no further real appreciation of the Swiss franc. It seems that the SNB has found the right approach to dealing with the world’s strongest currency. Supported by the SNB’s monetary policy, stable public finances, and continued international confidence

in the Swiss economy, the Swiss franc will remain a safe haven in the future.

The Economy

The Swiss economy has shown robust and stable development for several years – despite global uncertainties. The economy is heavily export-oriented, particularly in the pharmaceutical, chemical, and mechanical engineering industries. The strong Swiss franc brings with it both advantages and disadvantages: on the one hand, it makes imports cheaper; on the other, it affects the competitiveness of exporting companies. Despite the strong franc, however, there has been no sustained weakening of the export industry. This is due to high quality, reliability, and innovative strength. In addition, many international partners value Switzerland as a reliable, neutral, and stable business location – and are willing to pay a higher price for that. Like the Swiss franc, the Swiss economy is also characterised by its resilience and adaptability – and will continue to be one of the best-performing economies in the world despite global uncertainties.

Bonds

In May, inflation fell below 0 percent (-0.1 percent year-on-year), officially marking the Swiss economy’s return to deflation. The main cause is imported deflation, which is attributable to the record-high Swiss franc. For this reason, the SNB was forced to return to a zero interest rate policy and lowered the key interest rate from 0.25 to 0 percent. A possible next step – entering negative territory – cannot be ruled out, particularly if the franc remains so strong. This outlook is positive for mortgage borrowers on the one hand, but negative for investors in

fixed-interest investments in CHF on the other. Ten-year Swiss government bonds are currently still yielding just under 0.4 percent p.a., while corporate bonds with a good credit rating and a term of five years are yielding around 1 percent p.a. – with a downward trend. Such yield prospects are not really attractive for private investors. An investment in so-called ‘unconstrained’ bond funds, hedged against currency risks in CHF, is an option here. These funds can invest ‘unconstrained’ in the entire bond universe and thus achieve significantly higher returns. For further information, please contact our investment advisors.

Equities

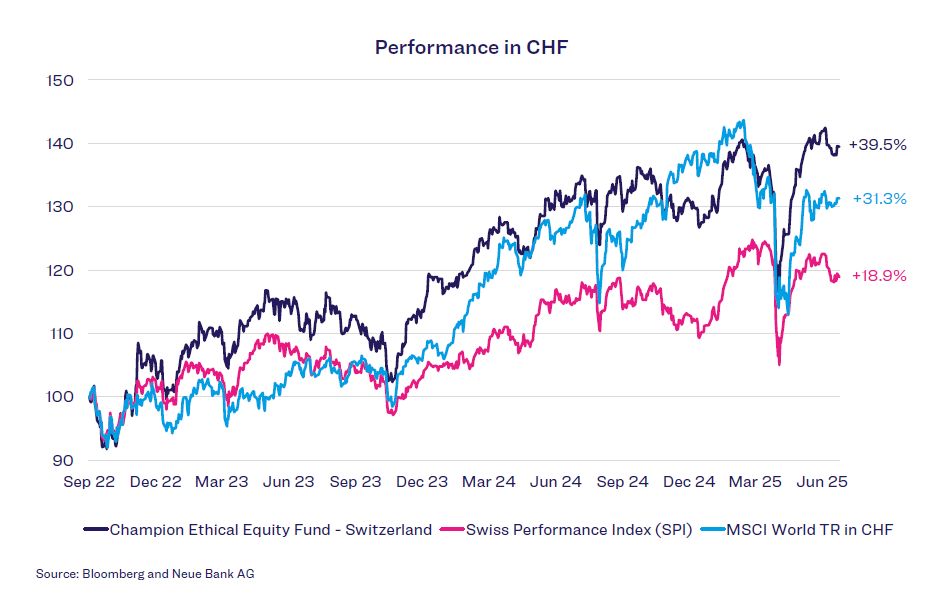

The low interest rates on the Swiss money and bond markets increase the relative attractiveness of Swiss equities compared to bonds. The equity risk premium is calculated by deducting the current yield on the bond market from the earnings yield on equities. At 5 percent, the Swiss equity market generates a significantly more attractive risk premium than the global equity market at around 2 percent, which supports a better future performance of Swiss equities. Added to this is the weak USD, which accounts for around 70 percent of the global equity market (MSCI World) and has lost around 12 percent in value against the CHF since the beginning of the year. This has had a noticeable impact on performance: while the MSCI World in USD has gained around 9.5 percent since the beginning of the year, performance in CHF remains negative at –3.8 percent. To exclude this currency risk and benefit from the higher equity risk premiums, an investment in Swiss equities is a good option. Since September 2022, we have acted as investment advisor to the Champion Ethical Equity Fund – Switzerland, in which we have implemented our equity strategy, successfully tested over many years. Since its launch, we have significantly outperformed the broad Swiss equity market (SPI) and the MSCI World in CHF:

For further information, please contact our investment advisors.

Alternative investments

Another beneficiary of lower key interest rates is the Swiss property market. It is known for its stability and security, which makes it attractive for both domestic and international investors. The Swiss economy is robust, interest rates are generally low, and property prices have proven to be relatively crisis-resistant in recent years. Nevertheless, there are also challenges and uncertainties that could influence the

market. In particular, rapid and sharp increases in key interest rates have a negative impact – as demonstrated by the year 2022, in which the SXI index for Swiss real estate funds lost almost 15 percent of its value. The losses have since been recouped, and the SXI is now at new highs. With the help of ETFs, investors can participate in the performance of the Swiss property market easily and cost-effectively.