Our responsibility

Sustainable and ethical action is a matter of course for us.

Learn more

Economy

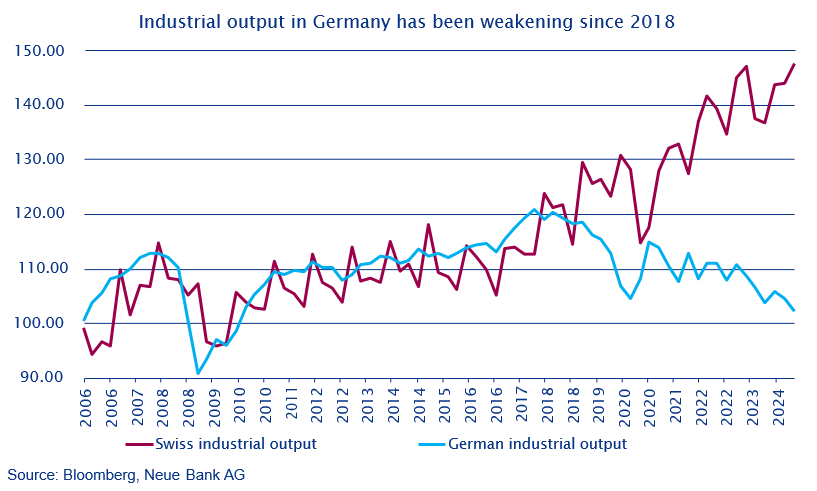

Germans and Swiss are said to have similar virtues – namely that they are punctual, hard-working, orderly and thrifty. The trade surplus consistently achieved by these two countries in this millennium – with a few exceptions – is another parallel. This is mainly due to the high demand for industrial goods abroad. Since 2018, however – i.e. even before the pandemic, the SPD-FDP-Green coalition government, and the Russian invasion of Ukraine – German industrial output began to weaken.

In terms of exports (latest available statistics), Switzerland is especially strong in the manufacture of chemical and pharmaceutical products (more than 50%), followed by machinery (approx. 13%) and watches (approx. 8%). In Germany, motor vehicles, motor vehicle parts, and other vehicles (approx. 20%) are the leading exports, followed by chemical and pharmaceutical products (approx. 16%) and machinery (approx. 14%). These different strengths can of course also have an impact on sales. For example, Switzerland managed to increase exports to the United States thanks to its strong pharmaceutical industry. Exports to the US are now higher than to Germany. The German automotive industry, on the other hand, is heavily dependent on China. For years, the Chinese market ensured high growth and abundant profits. Demand is now faltering – firstly, because the economic situation in China is not very rosy, and secondly, there is more demand for electric vehicles, for which the “Made in Germany” label is less of a selling point. Energy-intensive industries are suffering from the high electricity prices compared to the US and China, leading to an above-average decline in production in this segment. Higher taxes, excessive bureaucracy, the backlog in digitalisation, and neglected infrastructure are also having a negative impact. Switzerland, in contrast, benefits from stronger domestic demand, which was made possible not least by lower inflation, less pronounced interest rate hikes, and higher population growth. Nevertheless, Germany is still one of the most important customers for Swiss export goods. The German purchasing managers’ index for manufacturing fell to a new low of 40.3, which is also a worrying sign for Switzerland.

Currencies

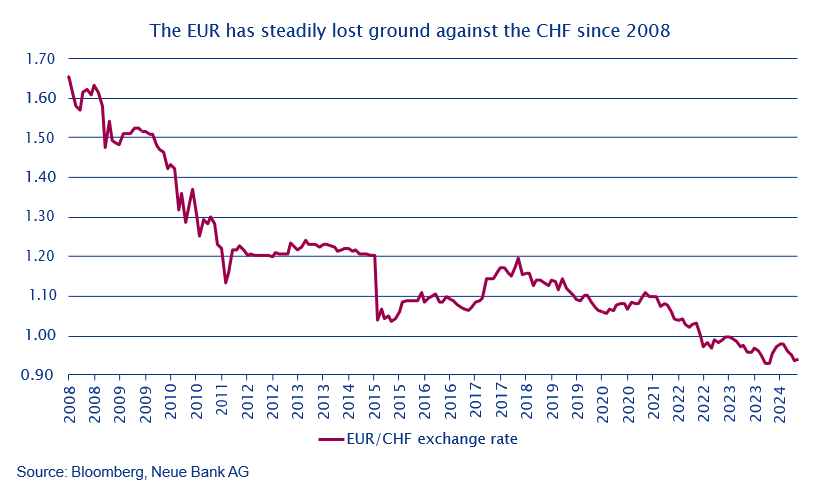

Germany does have one advantage over Switzerland: Since the financial crisis, German exporters have benefited from a weakening currency, which has made their production costs cheaper than those of their Swiss competitors.

Between 2011 and January 2015, the Swiss National Bank (SNB) attempted to put a stop to this competitive disadvantage by enforcing a minimum exchange rate of 1.20 on the market. This only succeeded in interrupting the trend, however. Some market observers even argue that the strong currency has always forced Swiss exporters to innovate more and make structural adjustments, putting them in a better position to withstand crises. Our EUR/CHF currency indicator has been pointing to a weakening EUR again since last month, after signalling at least a temporary recovery only just in March. Accordingly, we are now hedging EUR in our CHF reference currency portfolios.

Bonds

The weak economic data has now also prompted the US Federal Reserve (Fed) and the European Central Bank (ECB) to cut interest rates. Further interest rate cuts are expected. This has also led to both the USD and the EUR returning to a normal yield curve for the first time since 2022, which means that 10-year government bonds once again have higher yields than 2-year bonds. On the one hand, this represents normalisation – but it is also a typical leading indicator of a recession.

Equities

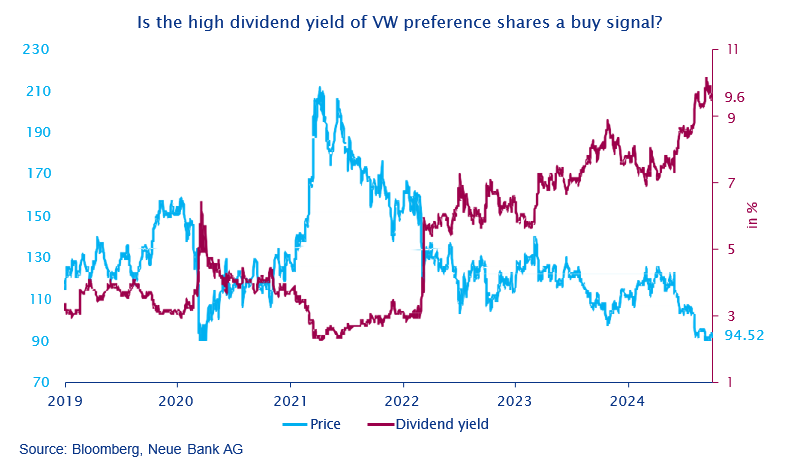

What sounds better, 10% dividend yield or 10% dividend growth? Those in favour of dividend yield should consider the following: a high dividend yield is often merely the result of falling share prices, as the example of VW preference shares in the following chart shows.

As long as a company does not see any attractive investment opportunities, it distributes profits to its shareholders. Money that is distributed can no longer be used for investments. Where there are no worthwhile investments, growth can no longer be expected. If a company is not growing, there is no reason for the share price to rise, and the value of the company actually falls due to the constant outflow of funds as a result of dividends. To stay with the example of VW, it generated a profit of EUR 27.02 per share in 2019 and paid out EUR 4.86 in dividends. This year, VW paid a dividend of EUR 9.06, and the profit estimates for the end of the year amount to EUR 27.19 per share. The ratio of distributions to profits is therefore increasing, leaving fewer funds for investments. The dividend yield is now 9.6%. Dividend yields this high are rarely sustainable and tend to be a harbinger of dividend cuts. An investment in VW preference shares would have resulted in a net loss of about 5% over the past 5 years (assuming automatic reinvestment of the dividend). In comparison, the DAX (German share index) rose by more than 50%. The price trend developed nearly in parallel until October 2022, but then the benchmark index surged and VW shares continued their correction. The dividend yield at that time was already around 7%. A financial analyst once described this as follows:

“A high dividend yield is a sign that a company was once great, but no longer is.”

Of course, VW might achieve a turnaround, and drastic cost-cutting measures have recently been announced. However, we are not bottom fishers who try to pick up shares lying at the bottom of the pond. We issued a sell recommendation on VW preference shares already a year ago, and before that the share had been underweight for several years. We prefer companies with sustainable dividend growth – which also answers our question at the outset.

Alternative investments

As we’ve already reported several times, gold has increased significantly in value this year – which is why we are focusing on silver in this issue. Gold and silver usually move in the same direction, with silver generally exhibiting the greater swings. This is one of the reasons why resourceful financial market observers came up with the gold/silver ratio. When the ratio is high, this has generally offered good entry opportunities for silver investments. Conversely, precious metals – and silver in particular – have generally lost ground when the ratio is low.

A look at the current situation shows that although the gold/silver ratio is not at its all-time peak, it is still at a historically high level. So if you want more momentum in your portfolio, you could consider investing in silver.